Regima

Portfolio construction and backtesting for retail investors — without the methodological shortcuts that make most backtests meaningless.

Regima is built around fixing that from the ground up.

The Problem

Most retail portfolio tools let you pick stocks, run a backtest, and show you impressive historical returns. What they don’t tell you is that the universe of stocks they’re testing against only includes companies that survived — companies that went bankrupt, got delisted, or were acquired have already been quietly removed. This is survivorship bias, and it systematically overstates every strategy’s historical performance.

What It Does

Users define a portfolio, choose an optimisation strategy, and backtest it against historically accurate market data — using point-in-time S&P 500 constituent datasets and fundamental data so the backtest reflects what was actually knowable at each decision point, not what looks obvious in hindsight.

Optimisation strategies:

- Mean-Variance Optimisation (MVO) — maximise expected return for a given level of risk, following Markowitz

- Risk Parity — allocate by risk contribution rather than capital, so no single position dominates the portfolio’s volatility

- Factor Tilts — tilt allocations toward systematic risk premia (value, momentum, quality) with configurable factor exposures

Backtesting engine:

- Point-in-time S&P 500 constituent universe — no survivorship bias

- Historical price action and fundamentals via yfinance

- Rebalancing at user-defined intervals

- Performance attribution across the full backtest window

Stack

| Layer | Technology |

|---|---|

| Frontend | SvelteKit |

| Backend | FastAPI |

| Database | PostgreSQL |

| Analytics | SciPy, SciKit |

| Data | yfinance, (more vendors to come) |

| Deployment | Docker |

Project Status

Partially built — working prototype exists for core optimisation and backtesting engine. Frontend and full deployment pipeline in active development.

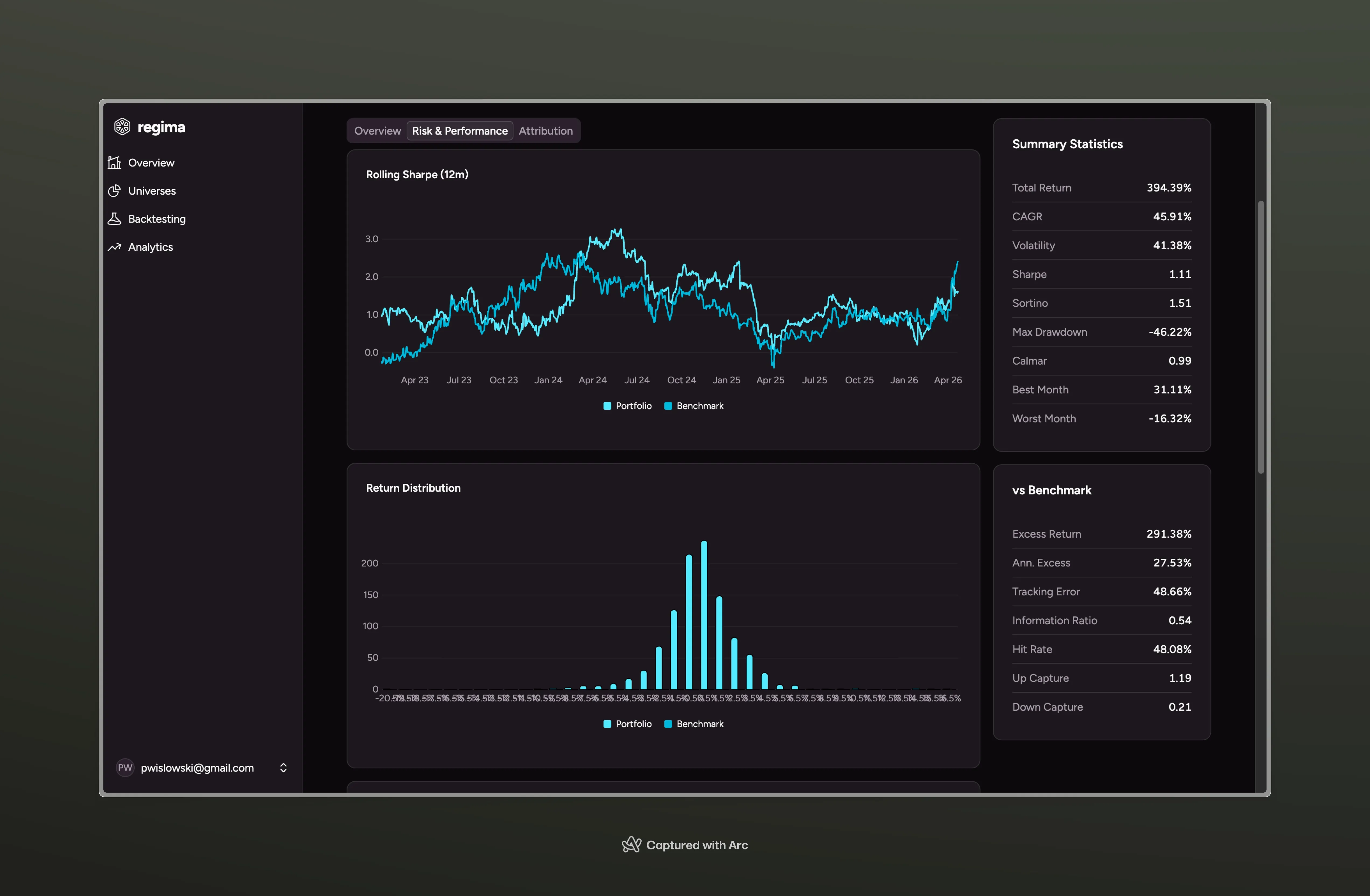

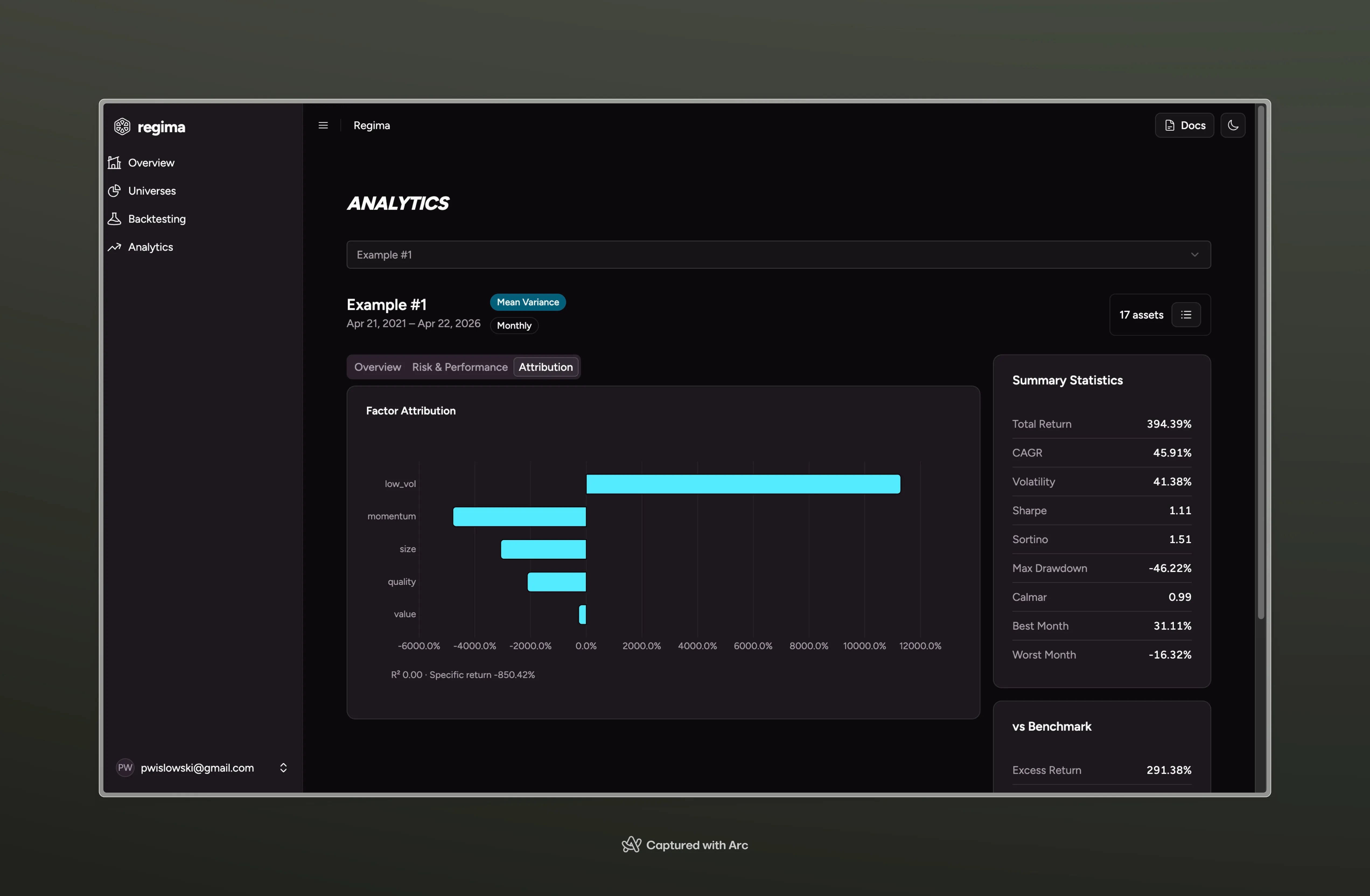

Screenshots of analytics

Performance

Risk analysis

Factor Analysis

Motivation

Built as a rigorous alternative to the shallow portfolio tools available to retail investors. The methodological decisions (point-in-time data, explicit bias controls, multiple optimisation frameworks) reflect the standards applied in professional investment management — made accessible without dumbing down the underlying finance.

Personally, I need a tool that provides me with seamless analytics out-of-the-box without reconstructing the same analytics pipeline over and over again. There’s a lot of comfort in knowing that your portfolio is rebalanced with optimization in mind. That is why I’m building Regima.

Roadmap

- Add benchmark comparison (vs. SPY, equal-weight)

- Portfolio-level risk decomposition (VaR, CVaR)

- Complete SvelteKit frontend

- Full Docker deployment

- Expand factor library

- Black-Litterman optimisation

- Minimum-variance optimisation

Author

Piotr Wislowski — passed all three CFA levels · MSc Business Statistics · Financial Engineer pwislowski.com · LinkedIn